.png)

.png)

You’re already thinking about saving, and that’s a powerful money move. Even better, you’re looking out for your future, finding ways to make your savings work harder, and keeping your credit score in mind. Nice work!

Here’s the short answer: no, opening an ISA won’t affect your credit rating.

An ISA is an “Individual Savings Account”, not a borrowing product like a loan, so it won’t appear on your credit report.

When you open one, your provider might run a soft check to confirm your identity, but that doesn’t leave a mark.

If anything, saving shows stability. Having money set aside in an ISA could boost your affordability (aka how much lenders think you can afford). Healthy financial habits show them you’re in control of your finances.

What is an ISA, exactly?

Short for “Individual Savings Account”, an ISA is a tax-efficient way to save or invest your money. Any interest on cash, or income and capital gains from investments in an ISA, are tax-free.

How are they tax efficient?

In the UK, most savers get what’s called a “Personal Savings Allowance” (PSA). It’s a small buffer that lets you earn savings interest before paying tax:

- Basic-rate taxpayers can earn up to £1,000 in interest and investment returns tax-free

- Higher-rate taxpayers can earn £500 before tax applies

Once you earn more than your savings allowance, any extra interest or returns outside an ISA can be taxed.

That’s where ISAs come in. Inside an ISA, your earnings from saving are tax-free. You don’t even have to declare the interest on a tax return.

That makes ISAs a great way to grow your money. Think of them like financial greenhouses that help you build up savings more quickly.

What kinds of ISA are there?

There are four main types of ISA:

You can also open a Junior ISA for people under 18 years old, with a savings limit of £9,000 in the 2025/6 tax year, a thoughtful way to help children and young adults build a savings habit early, and keep all their interest tax-free.

How much can I put into an ISA?

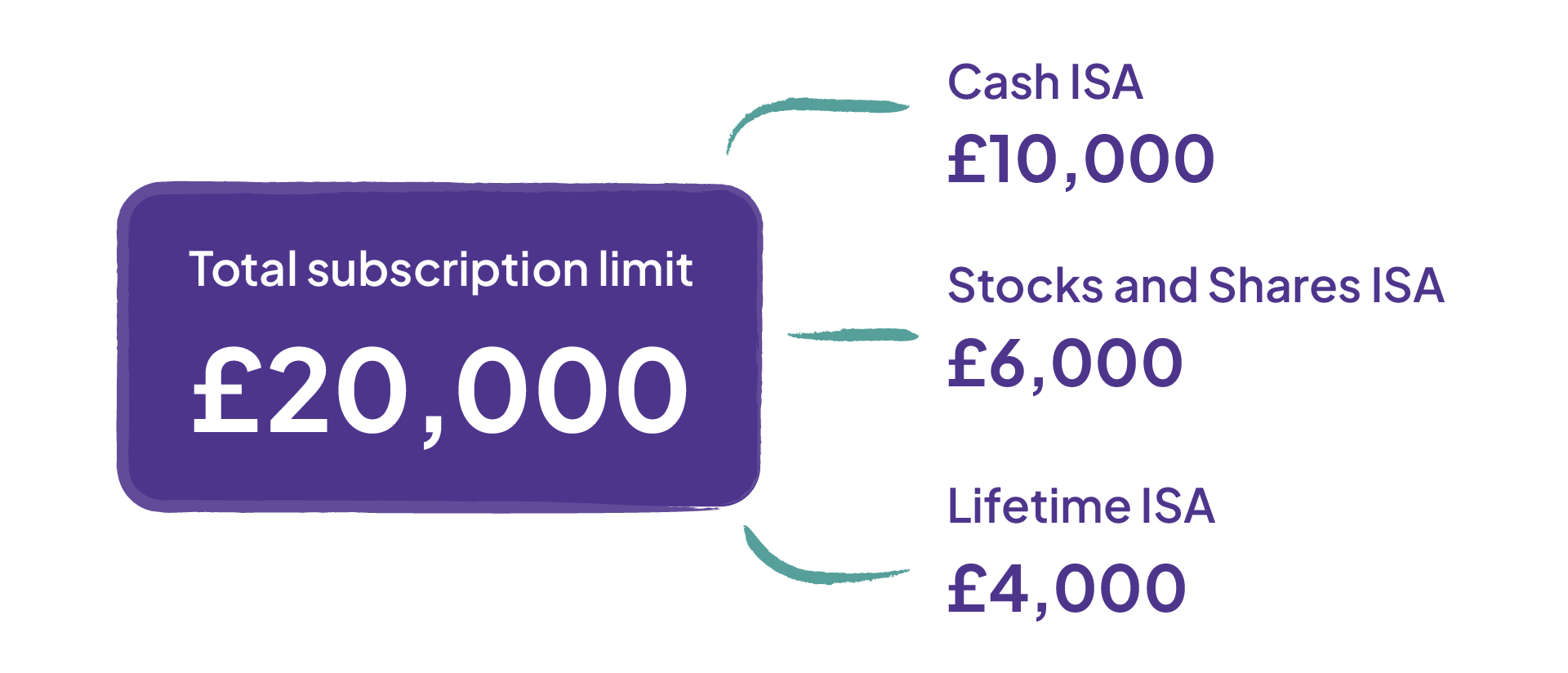

You can save up to £20,000 per person, each tax year (6th April - 5th April). The allowance is set by the government.

In April 2027, that amount will change to £12,000 for the under-65s, and you can save an additional £8,000 in stocks and shares ISAs.

However much you want to save, you have the flexibility to spread it across different ISAs. For example, £10,000 in a Cash ISA, and £6,000 in a Stocks and Shares ISA and £4,000 in a Lifetime ISA. It’s up to you how you want to use your allowance.

Some banks will show you how much allowance you have left to save, so keeping track of it is low effort, too.

If you ever manage to save more than that (wowza, go you!), you won’t be able to add more money to your ISAs. You’ll need to put money into a general savings or investment account, where any interest or returns over your £1,000 Personal Savings Allowance will be subject to tax.

How many ISAs can I have?

Every tax year, you can open and pay into multiple ISAs of the same type, as long as you stay within your £20,000 allowance.

That means more flexibility to shop around for better rates or mix providers to suit your goals.

Some ISAs are also “flexible”, meaning you can take money out and put it back in during the same tax year without losing part of your allowance. It’s worth checking your provider’s terms if you think you’ll dip into your savings during the year.

What if I go over the £20,000 ISA limit?

If you realise you’ve accidentally exceeded your £20,000, don’t panic. It happens, and it’s fixable.

If you make this mistake:

- Talk to your ISA providers as soon as possible

- They can talk to HMRC and help you sort out any potential tax issues

How to build credit while you save

Traditionally, saving doesn’t show on your credit report. But with Loqbox, you can grow your savings and build your credit score as you go.

Our savings feature isn’t an ISA, and won’t earn interest, but it lets you improve your credit while you save towards a goal. You could use it alongside your ISA or other savings products: earning interest on your other savings, while also using Loqbox to build your credit history month-by-month.

Choose how much you want to save each month, from £20, and build your credit as we report your savings payments to the UK’s three main credit reference agencies: Experian, Equifax, and TransUnion. Become a member today to access all of our powerful credit-building tools.

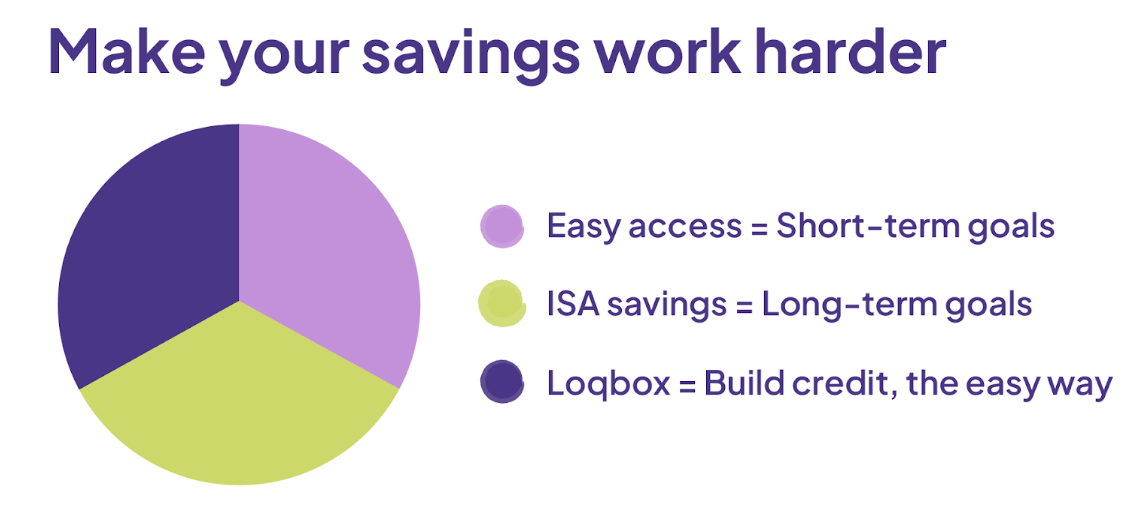

This is an example illustration of how you might divide your savings between different accounts, you could tip the scales depending on your goals:

Improvements to your credit score are not guaranteed. Missing payments to Loqbox or other credit accounts may harm your score.

.png)

.png)

.png)

.png)

.png)

.png)

.png)

.png)

.png)

.png)